The Digital

Lending Platform

Loan

Origination

The ApPello Loan Origination solution

supports the entire loan process from customer onboarding to highly-automated decision making and disbursement.

Loan

Servicing

ApPello’s Loan Servicing solution covers all possible requirements for banks of every size, from retail to large corporates, from start-up lending businesses to established loan providers.

Core Banking

Engine

ApPello’s digital Core Banking System (CBS) is a standalone cloud based, low code solution caters for current accounts, savings and lending functionalities. The Core engine is complemented by ApPello Digital Platform, AI tools and pre-integrated third-party solution.

What does

ApPello offer?

ApPello is a leading digital lending software platform vendor that has been providing end-to-end solutions from origination and servicing to collection for over 20 years.

The state-of-the-art ApPello Digital Lending Platform is currently one of the most powerful and prevalent in Europe.

The digitalization and digital transformation of lending processes using the latest technology is a core value of ApPello.

Our principle is to develop customer centric solutions that not only meet the business requirements,

but can also be easily configured by business users independently of an IT team. The Digital Lending Platform is provided primarily as an SaaS solution.

News &

Events

Up-to-date information for banking experts is a key to your company’s success. You can find here our thoughts, industry insights, white papers and much more.

/

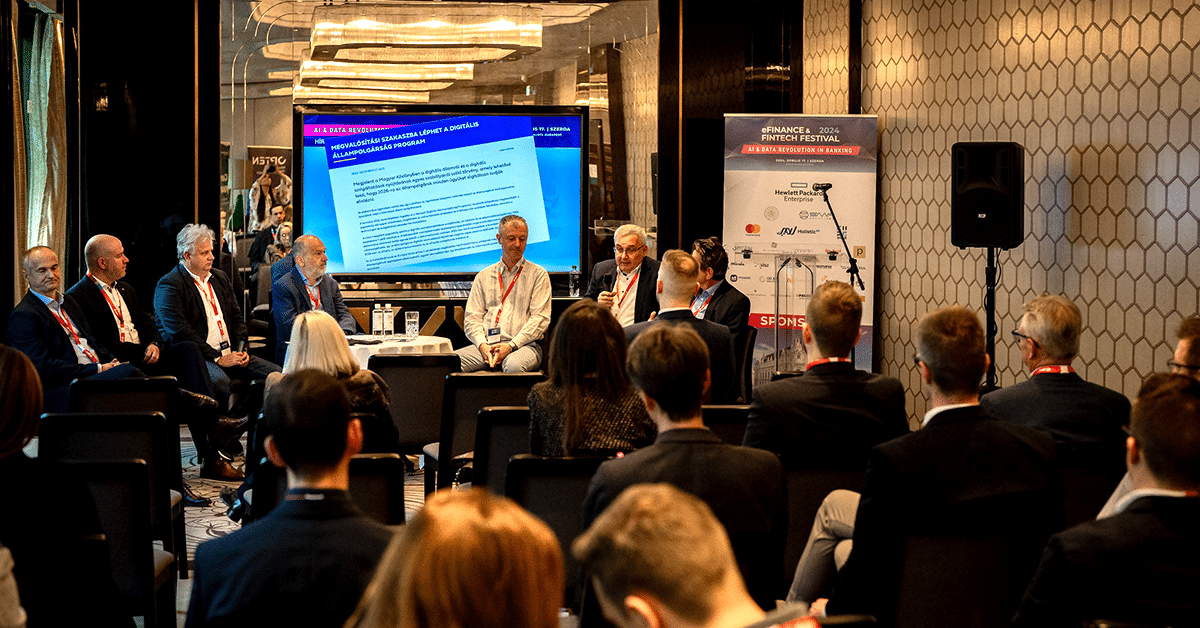

Hot topics of the conferences

Executives of ApPello took part at the AI Business Forum and eFinance & FIN/TECH Festival 2024

AI in the Banking Sector

Banking industry is undergoing a transformation fueled by advancements in AI technology.

Mortgage Loan Applications

The dream of a 15-minute mortgage loan application is no longer a distant fantasy but a reality on the horizon.

Trade Finance – now upgraded!

8 Steps of the Comprehensive Upgrade in ApPello Trade Finance Solution, Top technology WebDP platform

Stay up-to-date

Sign up for ApPello’s newsletter.

Our Customers’

success

ApPello has proven to be reliable, flexible and innovative partner.

Dita

Pasquier

Tribe lead,

Komercní Banka

As one of the leading players in the Hungarian housing savings and lending market, we consider it is very important to be among the leaders of business IT as well.

Attila

Soós

CIO/COO,

Member of the Board,

Fundamenta-Lakáskassza

The entire process has been a resounding success, greatly enhancing our operations and delivering exceptional results.

Roland

Pecsenye

Chief Digitalization Officer,

MBH Bank

…we have managed to significantly optimize the processes related to the collateral registry required by mortgage banking laws.

György

Máriás

Head of Operation,

K&H Jelzálogbank Zrt.

ApPello proved to be a great partner to develop digital channels to our corporate customers.

Dénes

Ozorai

CIO, ICT Development Directorate,

K&H Group

ApPello is a long term, trusted partner, that we could always count on.

János

Anschau

Head of Global Banking Services, UniCredit Bank

Working with ApPello, we’re building a credit infrastructure that allows us to maintain our market leadership position and grow our business.

Tamás

Foltányi

Executive Director,

Deputy CEO IT & Operating, Erste Bank

ApPello continues to be a trusted partner for CIB Bank

Sante

Cusimano

CIB Bank Ltd.

Intesa Sanpaolo Group

Chief Operating Officer

Member of CIB Management Board

Tenders

AI Scoring Engine

Successfully completed the unique end-to-end modelling platform, that enables the rapid design and deployment of high performing AI models.